Traditionally, the most common way to pass down family wealth has been by way of discretionary trust structures. However, recent changes to the tax regime now mean that family investment companies (FICs) could offer more favourable tax treatments when deciding how to deal with future generations – particularly for individuals with large inheritance tax (IHT) estates.

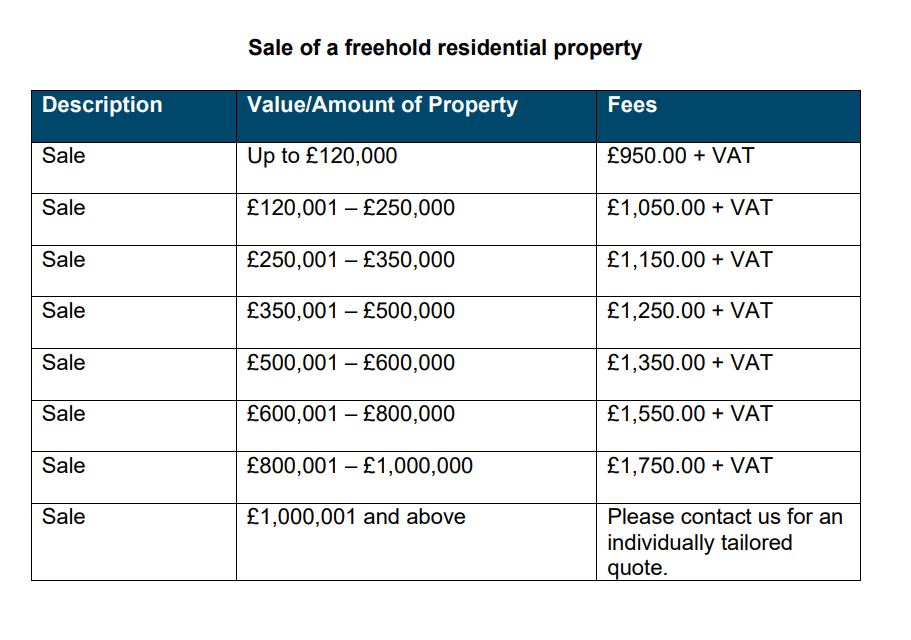

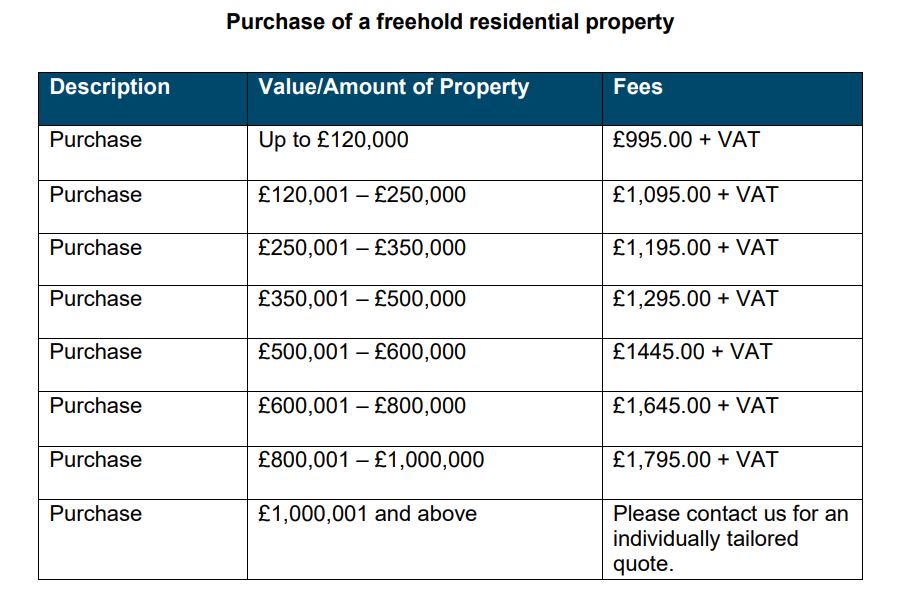

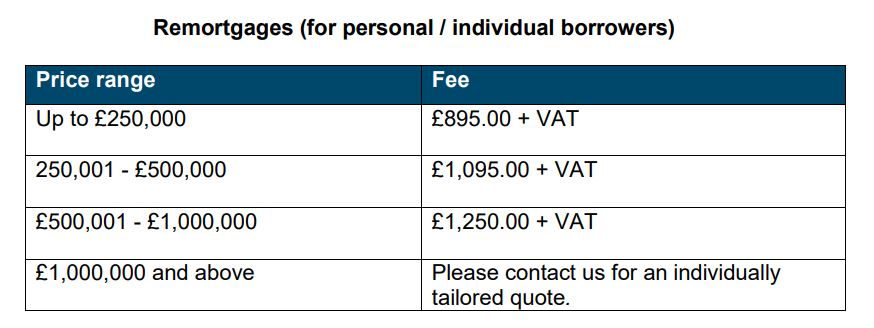

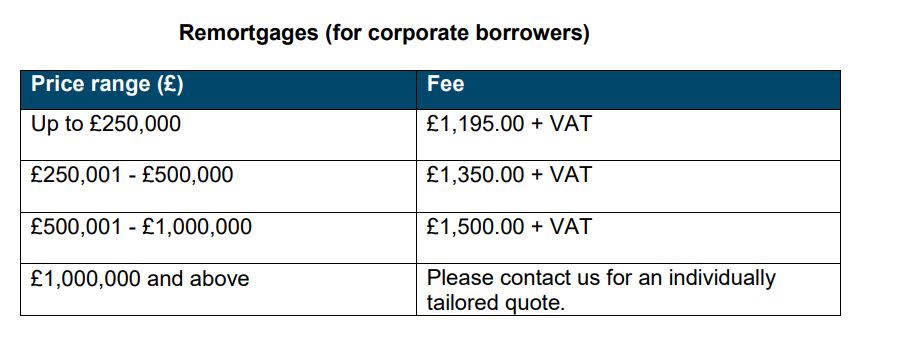

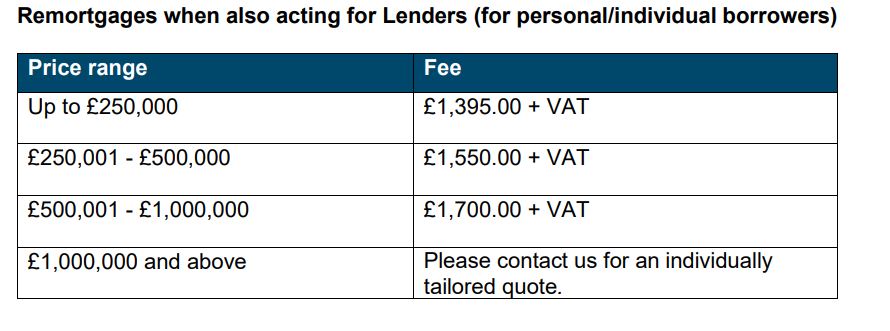

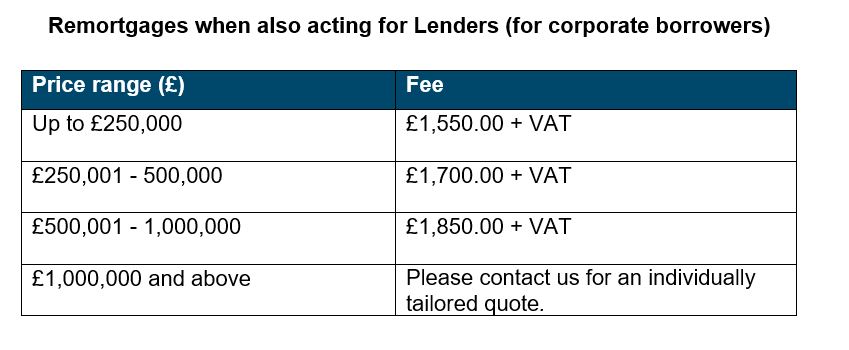

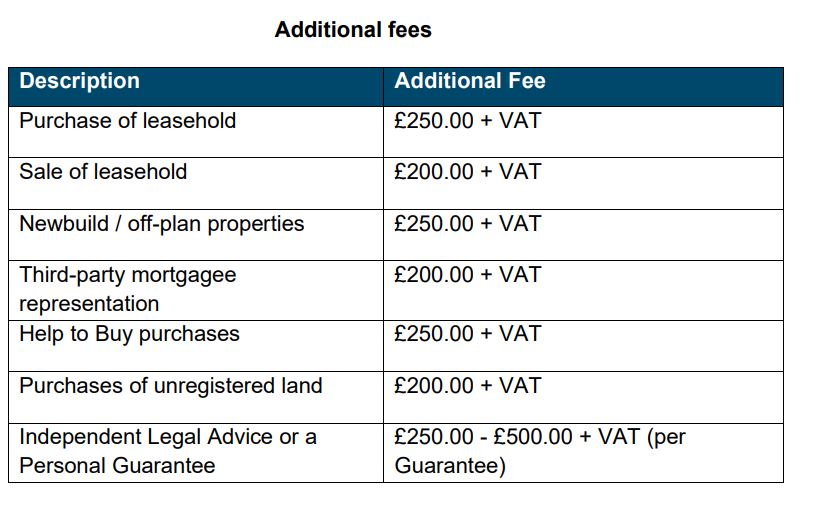

Bermans property team offer a personal conveyancing service for the following types of residential property:

Freehold sale or purchase

Leasehold sale or purchase

Mortgages or re-mortgages

Our conveyancers are experts in guiding you through the legal process and you can be safe in the knowledge that they are supported by our larger commercial property team.

Whether you are buying or selling or refinancing we can provide you with cost certainty and confidence that you are in safe hands.

We provide a list of our headline rates below but we like to provide a specific quote to suit your needs so do get in touch and we will provide a fixed fee quotation.

PLEASE NOTE

These fees exclude disbursements and any Stamp Duty Land Tax payable to HM Revenue and Customs.

The holiday season might have ended, but holiday pay remains a hot topic. In Flowers v East of England Ambulance Trust, the Employment Appeal Tribunal looked at whether voluntary overtime should be included in holiday pay. Employees should be paid their ‘normal remuneration’ when they take holiday. But is voluntary overtime ‘normal’ pay?

Mr Tabberer and his colleagues were electricians. They were originally employed by Birmingham City Council. Their employment transferred several times by way of TUPE (Transfer of Undertakings (Protection of Employment) Regulations 2006) over the years. At the time of the tribunal claims, they were employed by Mears. The employees were contractually entitled to receive an Electricians’ Travel Time Allowance, though the historical reasons for the allowance no longer existed. Mears varied the employees’ contracts to remove the allowance, saying it was outdated.

Our pricing for bringing and defending claims for unfair or wrongful dismissal (excluding disbursements and Counsel’s fees).

Simple case: £8000 to £10,000 (excluding VAT)

Medium complexity case: £10,000 to £20,000 (excluding VAT)

High complexity case: £20,000 to £75,000 (excluding VAT).

Factors that could make a case more complex:

If it is necessary to make or defend applications to amend claims or to provide further information about an existing claim

Defending claims that are brought by litigants in person

Making or defending a costs application

Complex preliminary issues such as whether the claimant is disabled (if this is not agreed by the parties)

The number of witnesses and documents

If it is an automatic unfair dismissal claim e.g. if an employee is dismissed after ‘blowing the whistle’ on his/her employer

Allegations of discrimination which are linked to the dismissal

Disbursements

Disbursements are costs related to your matter that are payable to third parties, such as medical experts. We handle the payment of the disbursements on your behalf to ensure a smoother process.

Counsel’s fees

We would generally instruct a barrister to represent you at the Employment Tribunal hearing. Barristers’ fees are broken down into two areas: i.) a Brief fee, which covers their preparation for the hearing and the first day of the hearing and ii.) a Refresher, which covers each additional day after the first day of the hearing. Brief fees are estimated to be between £850 to £5000 plus VAT (depending on the level of experience of the Barrister, the complexity of the case and the length of the hearing). Refreshers are estimated to be between £700 to £1250 plus VAT (depending on the level of experience of the Barrister).

Key stages

The fees set out above cover all of the work in relation to the following key stages of a claim:

Taking your initial instructions, reviewing the papers and advising you on merits and likely compensation (this is likely to be revisited throughout the matter and subject to change)

Entering into pre-claim conciliation where this is mandatory to explore whether a settlement can be reached;

Preparing claim or response

Reviewing and advising on claim or response from other party

Exploring settlement and negotiating settlement throughout the process

Preparing or considering a schedule of loss

Preparing for (and attending) a Preliminary Hearing

Exchanging documents with the other party and agreeing a bundle of documents

Taking witness statements, drafting statements and agreeing their content with witnesses

Preparing bundle of documents for the Tribunal hearing

Reviewing and advising on the other party’s witness statements

Agreeing a list of issues, a chronology and/or cast list

Preparation and attendance at the Final Hearing, including instructions to Counsel

The stages set out above are an indication and if some of stages above are not required, the fee will be reduced. You may wish to handle the claim yourself and only have our advice in relation to some of the stages. This can also be arranged on your individual needs.

How long will my matter take?

The time that it takes from taking your initial instructions to the final resolution of your matter depends largely on the stage at which your case is resolved. If a settlement is reached during pre-claim conciliation, your case is likely to take four to six weeks. If your claim proceeds to a Final Hearing, your case is likely to take between six and twelve months. This is just an estimate and we will of course be able to give you a more accurate timescale once we have more information and as the matter progresses.

Contact us to speak to a member of the employment team.

An employee ownership trust (EOT) is a trust established for the benefit of the employees of a business. Selling a majority stake in your company to an EOT will mean that your employees will have an indirect interest in the business, potentially leading to increased performance and commitment, as well as a number of additional benefits:

A disposal of a majority shareholding in a company to an EOT will generally be free of capital gains tax, income tax and inheritance tax.

Bonus payments of up to £3,600 per year can be made to employees of the business, tax-free.

Full market value for the shares can be realised by the selling shareholders.

The shareholders do not have to sell all of their shares, so can continue to have a stake in the business, and can remain as directors of the company post-sale.

In order to sell shares to an EOT and realise the benefits outlined above, a company (which must be a trading company or a holding company of a trading company) will usually be incorporated to act as the trustee of the EOT. The relevant company and the EOT trustee will enter into a trust deed, under which the property held by the EOT trustee, such as the shares in the company, are held for the benefit of the company’s employees.

The company’s shareholders will then agree to sell more than 50% of the shares in the company to the EOT Trustee. Depending on how the transaction will be funded, the purchase price may be left payable on deferred terms so as to allow the dividends received by the EOT trustee from the trading company to be used to pay the purchase price.

What is required to qualify?

In addition to the requirement that the relevant company must be a trading company, there are certain additional requirements which must be met in order for the transaction to qualify for the tax treatment benefits:

The “all-employee benefit” requirement. The terms of the trust must not permit the trust property to be applied other than for the benefit of all the business’ employees, to transfer the property to another trust, or to make loans to the trust beneficiaries.

The “equality” requirement. Any distribution from the trust fund, or payment under a bonus scheme, must be for the benefit of all eligible employees, on the same terms.

The “controlling interest” requirement. The EOT trustee must hold at least 50% of the ordinary share capital, voting rights, profit entitlement and entitlement to assets on a winding-up.

What are the benefits?

You will appreciate this tax-efficient structure provides another exit opportunity to management alongside trade sale, traditional MBOs (VIMBOs, MBIs, etc.), listings and asset sales. This allows management partially to de-risk their investment and unlocks tax-free capital to invest elsewhere.

Bearing in mind the succession issues experienced by owner-managers since the financial crisis of 2008, this structure is well worth considering as part of clients’ financial planning.

This structure is also well suited to professional service firms where ownership and capital value may be barred due to the high cost of buy-in. Using this method would incentivise and tie in valuable members of teams and ensure a fruitful final exit for management and employees

How can we help?

If you would like to discuss the benefits of implementing an EOT structure, we would be happy to discuss it further with you. Bermans can assist in all aspects of the transaction, including:

Setting up the company to act as the trustee of the EOT.

Preparing the trust deed between the company and the EOT trustee, detailing the terms on which the company’s shares will be held for the benefit of the employees.

Preparing the constitutional documents of both the company and the EOT trustee.

Drafting and advising on the share purchase agreement relating to the sale of the shares to the EOT trustee.

Advising on any documents or structures relating to the funding of the transaction.

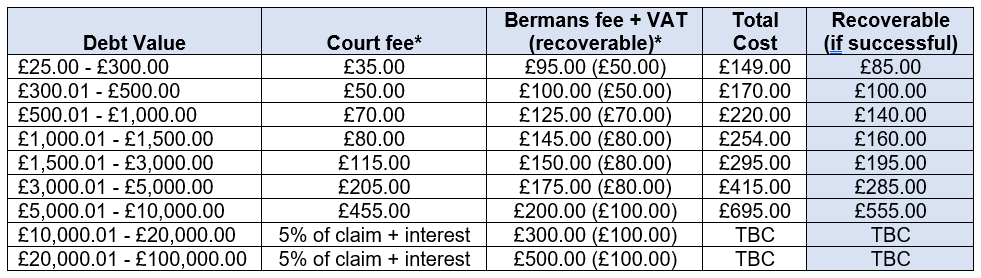

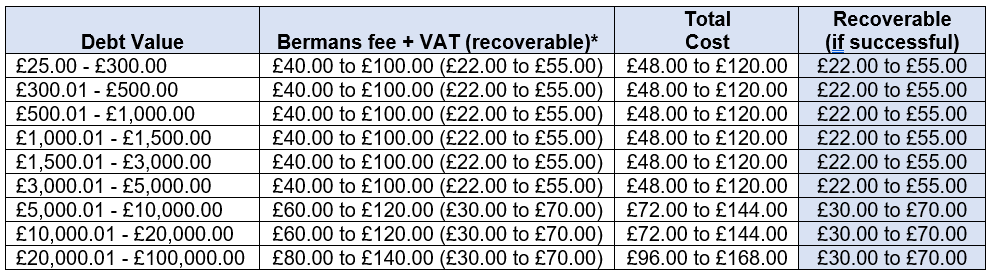

This includes taking instructions, preparing and issuing letter by 1st Class post.

The debtor will be advised to send any payments and communication to you directly.

Should you require us to enter into discussion or correspond with the debtor this would be carried out at a standard additional fixed fee of £30.00+VAT per item.

A fee of £10.00+VAT is chargeable for transferring each debtor payment received by us to you.

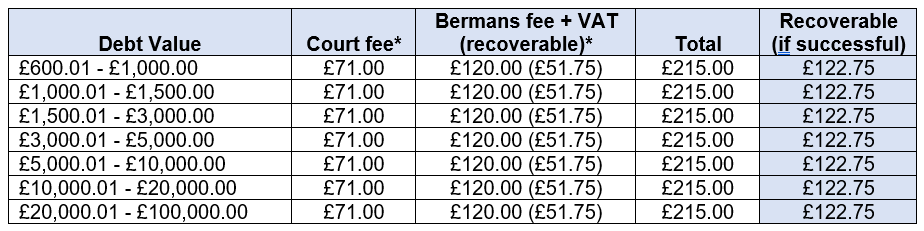

Stage 2 – Issue of Claim

*Both the Court fee and part of Bermans fee (as shown in brackets) are recoverable if successful

Should the debtor file a defence then this will be referred to one of our lawyers who will advise you accordingly. Any work carried out at this point will be chargeable at an hourly rate, as detailed later in this document.

Stage 3 – Obtain Judgment

*Part of Bermans fee (as shown in brackets) is recoverable if successful

The £ value range given above is dependent on the type of Judgment being requested:

In default of Acknowledgement of Service

In default of Defence

On Admission and acceptance of offer

On Admission and rejection of offer

Stage 4 – Enforcement

Writ of Control (enforcement via HCEO)

*Both the Court fee and part of Bermans fee (as shown in brackets) are recoverable if successful

Should enforcement be unsuccessful the HCEO will charge an abortive fee of £75.00+VAT.

Costings for other forms of Enforcement are available on request (as below):

The Government recently announced that it does not intend to legislate to implement the September 2016 Law Commission proposals to modernise the archaic Bills of Sale regime:

“Given the concerns that were raised in the consultation, the small and reducing market and the wider work on high-cost credit, the government will not introduce legislation at this point in time. The government will continue to work with the FCA as they carry out their high-cost credit review, and then further consider government action on alternatives to high-cost credit in light of the FCA’s review”.

The Law Commission is reviewing the difficult subject of the electronic execution of documents, and in particular deeds.

In principle all legal documents should be capable of electronic execution, but some doubt remains about the position regarding deeds in view of the statutory requirement for deeds to be witnessed.

|

|

Traditionally, the most common way to pass down family wealth has been by way of discretionary trust structures. However, recent changes to the tax regime now mean that family investment companies (FICs) could offer more favourable tax treatments when deciding how to deal with future generations – particularly for individuals with large inheritance tax (IHT) estates.

Traditionally, the most common way to pass down family wealth has been by way of discretionary trust structures. However, recent changes to the tax regime now mean that family investment companies (FICs) could offer more favourable tax treatments when deciding how to deal with future generations – particularly for individuals with large inheritance tax (IHT) estates.