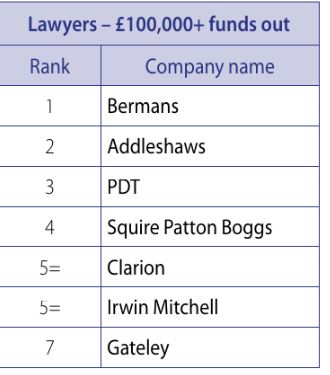

In April 2019, Bermans topped the professional poll for choice of legal services for both +£100k and sub £100k funds out in Business Money’s report of the UK invoice finance sector.

The professionals poll rankings are voted for by asset finance providers who are asked about their choice of professional when acquiring a lawyer amongst other professional sectors.

The summary quotes:

“If Bermans was the only law firm to make a significant showing in the sub-£100,000 category it also topped the £100,000 funds out poll amongst a dozen finance houses.”

On 1 April 2019 the jurisdiction of the Financial Ombudsman Service (“FOS”) was extended to include additional categories of eligible complainants such as more SMEs and individual guarantors of loans. The FCA has also indicated that it intends to increase the limit of an award which can be made by the FOS under its compulsory jurisdiction scheme from £150,000 to £350,000, probably sometime later in 2019.

The Credit hire and credit repair industries and ancillary services provided to claimants in “no fault” accidents have traditionally been regarded as challenging sources of business for invoice financiers, but there are signs that financiers are becoming more comfortable with the risks involved.

It is fair to say that these industries have over recent years been subject to a number of measures by the Government in attempts to reduce overall insurance premiums, but they continue to display a sense of innovation.

The recent decision by one of the main bank owned invoice financiers to withdraw from the provision of credit protection has highlighted a continuing debate within the industry on issues arising from the interface between bad debt protection on the one hand and the provision of insurance on the other hand.

It is now widely understood within the industry that the provision of insurance is a regulated activity under the Financial Services and Markets Act 2000 (“FSMA”) which requires providers to be authorised and regulated by the Financial Conduct Authority.

There are various ways in which a business can protect its business interests whether that is profit or cashflow. Many will look first at the internal workings of the business to make savings and some may never look at their other options with external parties. Having in place contractual provisions which assist you in that regard are often overlooked. The aim of this article is to provide some ideas on how a business can protect itself in these uncertain times.

Liquidation is the procedure through which the assets of a company are realised and distributed to creditors to satisfy the company’s debts in accordance with the Insolvency Act 1986. At the end of this procedure the company is dissolved and no longer exists. The process is often referred to as winding up a company.

Liquidation can happen in isolation, for example if there is no prospect of selling the company, but it can also follow as an exit route for a company in administration. In 2018 over 15,000 companies were liquidated.

There are two types of liquidation; voluntary liquidation and compulsory liquidation.

Voluntary Liquidation

Voluntary liquidation can be achieved in two ways:

Members’ voluntary liquidation – this option can be used if a company is able to pay its debts but the management have decided to wind up the company, for example on retirement.

Creditors’ voluntary liquidation – if a company is unable to pay its debts then a creditors’ voluntary liquidation is the process to follow to wind up the company.

Compulsory liquidation

A compulsory liquidation comes about as a result of the court granting an order to wind up the company, most likely on the petition by HM Revenue & Customs of one of the company’s other creditors.

The Role of the Liquidator

The liquidator has wide ranging powers including to collect and realise assets, to disclaim onerous property, to pursue or defend legal proceedings and to challenge antecedent transactions.

What to do next?

If you think your company is in danger of being liquidated, has received a winding up petition or if you are considering exit strategies that include liquidation, it is important to seek professional advice.

We act for liquidators, creditors and companies in relation to the liquidation process. We can offer practical and commercial advice as well as giving you expert advice on your legal position.

Prior to 2002, creditors holding a charge over a company’s assets (usually a bank), had the right in certain circumstances to appoint a receiver. A receiver was an Insolvency Practitioner who acted on behalf of the creditor. Its duty was to take custody of the company’s assets and exercise powers with a view to satisfying the debt owed to the creditor.

In 2002 the law changed and restricted the use of this procedure to certain types of companies or floating charges created prior to September 2003. For this reason, administrative receiverships are rare (in 2018 there were only a handful in the UK).

LPA Receivership and Fixed Charge Receivership

LPA receiverships and fixed charge receiverships are different to administrative receivership.

Under the Law of Property Act 1925 (LPA), creditors (usually banks/lenders) that hold a fixed charge over property have a statutory right to appoint an LPA receiver.

A fixed charged receivership is when a creditor who has a fixed charge over a company’s assets, has the power under the terms of the security documentation to appoint a receiver.

In these situations the receiver will have powers to help realise the debt owed to the creditor by taking charge of the assets/property. This could mean selling the assets that are the subject of the charge or managing them and collecting the rent for the benefit of the lender.

What can you do if a receiver is appointed in respect of your company’s assets?

We are experienced in advising both lenders in respect of the appointment of receivers, receivers in relation to legal issues arising from the exercise of their powers and companies facing receivership which gives us valuable experience in advising on this specialist area.

If you receive a formal demand from a lender indicating their intention to appoint a receiver, or a receiver has been appointed in respect of your company, it is critical that you seek urgent advice.

We regularly advise companies on the validity of the appointment of a receiver, their rights and the best course of action. We offer practical, commercial advice rather than just restating the law.

We act for insolvency practitioners, lenders and business owners on all aspects of corporate restructuring and insolvency.

Our client base includes a number of North West based and nationally based insolvency practitioners, most of whom we have advised for many years. They welcome our practical and commercial advice and our responsiveness. We advise them on the full range of insolvency processes.

Where commercial lenders have clients who are struggling to pay their debts, or are involved in an insolvency process, we assist the lenders in recovering their funds.

When businesses are having financial difficulties, we are able to advise the owners on the best solutions for their situation, whether that be a formal process such as administration, or an informal restructuring, a managed turnaround and refinance or just general commercial and practical advice.

We also regularly advise purchasers who are buying distressed businesses that may or may not be in an informal insolvency process.

There are a range of procedures available to struggling businesses including:

Insolvency is defined in the Insolvency Act 1986, but broadly it means when a company does not have sufficient assets to discharge its liabilities as they fall due.

If this occurs, there are options open to the company owners and other stakeholders, one of which is administration. Administration is an insolvency process where an insolvent company is placed under the control of an insolvency practitioner (IP) to enable the IP to achieve objectives laid down in legislation.

How does a company enter administration?

There are two ways for a company to enter administration:

By court order – an application for a court order can be made by creditors i.e. those owed money by the company, the company itself, its directors, a liquidator, a supervisor of a CVA or pursuant to legislation.

By an out of court process by lodging certain documents with the court – this process is only available to the company or its directors or a party with a qualifying floating charge (usually a bank or commercial lender).

Why would a company or its directors put it into administration?

From the date that an application is made to court or a notice of intention to appoint administrators is filed, a moratorium in respect of claims will apply to protect the company against actions from creditors. In general terms this means that creditors will not be able to issue proceedings, HMRC will not be able to distrain or issue a winding up petition against the company and the landlord will not be able to forfeit its lease. If the company is concerned that creditors may issue proceedings then administration can provide some short term protection, allowing the company to restructure.

Often companies that enter administration end up being sold or at least their businesses and assets do. Sometimes a sale is agreed prior to the company going into administration and it may be a term of completing the sale that the company is put into administration first. Such sales are known as pre-packs. Pre-packs can be a relatively quick and smooth way to continue the business with as little disruption as possible.

What are the objectives of the administration?

The first objective of an administrator is to rescue the company so it can carry on as a going concern.

If this isn’t possible then the aim is to achieve a better result for the company’s creditors than would be likely if the company was put into liquidation. If such a better result cannot be achieved, then the objective is to realise the property of the company and distribute the proceeds to the company’s secured and preferential creditors in the first instance.

Next steps

If your company is experiencing financial difficulties and you are considering administration please get in touch. We can provide initial advice about your restructuring options and introduce you to an IP.

If you are considering purchasing a business or assets from an administrator, please get in touch. We have a wealth of experience in structuring pre-pack sale agreements and advising individuals and companies on purchases of distressed businesses and assets

|

|